Pellom Capital Preservation LLC Q3 2024 Facts, Figures and Ideas

Pellom Capital Preservation LLC is a private family office registered in the state of Tennessee. Pellom Capital Preservation LLC is not a registered investment advisor with any governing or regulating body. Nothing in this website should be construed as a public offering or solicitation. We do not accept outside funds for our services. We are not professional investment advisors nor do we represent ourselves as such.

The information on this site is not intended to be and should not be treated as legal advice, investment advice, or tax advice. You should discuss all recommended tax strategies and other strategies that may be available to you with your professional investment, legal and accounting advisors before implementing them.

Hello everyone!

Excited to put a bow on Q3 2024, our first quarter in business. It is nice to have verifiable performance numbers to track, even if the news is good, bad or indifferent.

The best way to do this is to share the results of our “Default Portfolio” vs. various benchmarks over the past three months. If you’d like to read more about our Default Portfolio, you can do so here:

Pellom Capital Preservation Default Portfolio

"There’s no such thing as a perfect portfolio, strategy or asset allocation, so I’m all about figuring out what works for your personality and sticking with the process you choose." - Ben Carlson

I will also share my thinking on the default portfolio vs. how I manage my own personal investments.

Pellom Capital Preservation Default Portfolio

Please remember the intention of this portfolio is to serve as an “all weather” portfolio. What that means, to us anyway, is that it can perform well in all market conditions without chasing performance risk.

Here are the target allocation amounts:

VTI Vanguard Total Stock Market ETF - 30%

BND Vanguard Total Bond Market - 25%

OUNZ VanEck Merk Gold ETF - 20%

BRK.B Berkshire Hathaway - 12.5%

MKL Markel - 12.5%

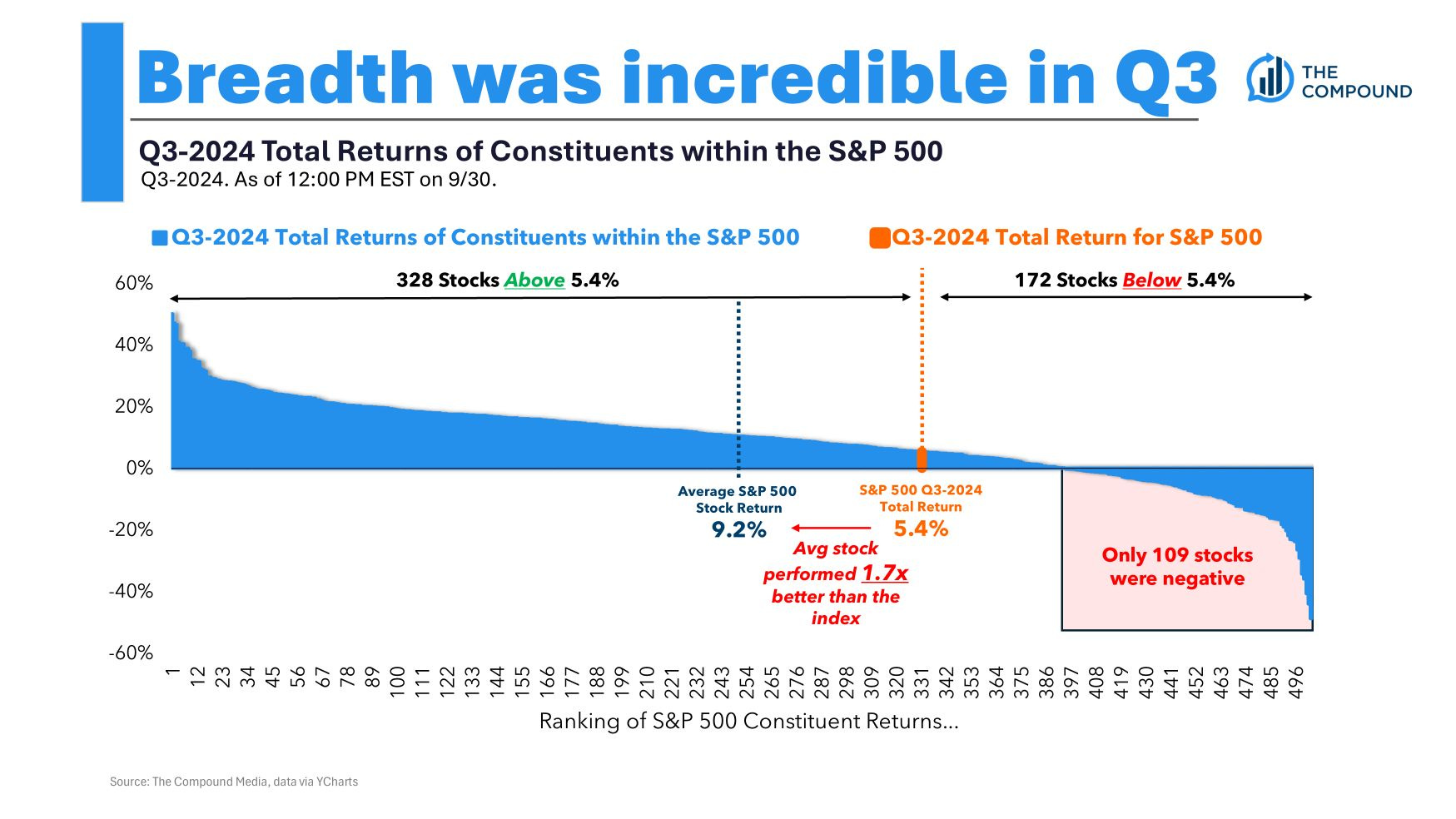

Like the stock market as a whole, the above portfolio had a great quarter. As of the close of business on September 30th, the portfolio increased 7.17%. Berkshire Hathaway was on fire, up 13.59%. Gold ripped higher as well, up 12.74%. VTI rose 5.64%, BND rose 5.12%. Markel was the only drag on performance, losing 0.43% over the past three months.

The S&P 500 was up 5.40% over the same span.

Tyler’s Personal Portfolio

Here’s how I think about my personal portfolio vs. the default portfolio above I recommend to friends and family. William Green was recently on the The Value Perspective Podcast. Here’s the link if you’re interested:

This conversation covered multiple topics, but William said something I totally agree with regarding the idea of being a “stock picker” vs. an index investor. I’m paraphrasing, but William admitted he invests in index funds in the accounts he manages for his wife and children. He said, “why should my family be beholden to my ego that I think I can pick stocks and beat the market?” He knows the statistics say he can’t do it. I know the statistics say I can’t do it.

There is a natural fiduciary responsibility in managing and advising family members. You want them to do well for their own sake. You shouldn’t need them to do well so long as the process glorifies you in the process.

I am a non-professional investor using a combination of my education, experience, temperament and personal interests in an effort to help grow family money. As such, it would be asinine and selfish to expect others to follow me and my investment decisions with impunity.

I share my portfolio decisions here in an honest attempt to gain skill and knowledge by forcing myself to be publicly accountable for my actions. I do not claim to be an expert. You should not blindly follow anything I post without doing your own due diligence and research. If you are looking for someone to echo, there are much better singers in the world, that I can promise.

Earlier in the month I wrote about my investing edge, or lack-thereof:

Edge

I’ve been kicking this idea around in my head for a while. I think there are essentially only two edges a small investor, whether they be an individual or professional managing a limited amount of assets, can have over the market.

I believe I can identify undervalued companies. I believe I have the temperament to buy and hold even when the results are temporarily going against me. I believe my ability to invest money I don’t plan to use for 30, 40 or 50 years gives me a perspective that allows for outperformance. I believe one does not have to be a genius to benefit from compound interest.

I don’t believe I can anticipate where the stock market is going over the next three days, three months, or three years. I don’t believe I can predict which companies will grow their earnings exponentially over time. I won’t see the next big thing coming. I won’t be on the forefront of new technologies or cultural trends.

Knowing my strengths and weaknesses, it’s not hard to see how the value investing framework is the only framework available to me. It boils down to attempting to buy a dollar for fifty cents and holding the gain as long as possible. Don’t misunderstand this as a guarantee of future success. I am learning by doing in real time.

Here are the companies I own:

BRK.B Berkshire Hathaway - 15%

Berkshire Hathaway Inc., through its subsidiaries, engages in the insurance, freight rail transportation, and utility businesses worldwide. The company provides property, casualty, life, accident, and health insurance and reinsurance; and operates railroad systems in North America. It also generates, transmits, stores, and distributes electricity from natural gas, coal, wind, solar, hydroelectric, nuclear, and geothermal sources; operates natural gas distribution and storage facilities, interstate pipelines, liquefied natural gas facilities, and compressor and meter stations; and holds interest in coal mining assets. In addition, the company manufactures boxed chocolates and other confectionery products; specialty chemicals, metal cutting tools, and components for aerospace and power generation applications; flooring products; insulation, roofing, and engineered products; building and engineered components; paints and coatings; and bricks and masonry products, as well as offers manufactured and site-built home construction, and related lending and financial services. Further, it provides recreational vehicles, apparel and footwear products, jewelry, and custom picture framing products, as well as alkaline batteries; castings, forgings, fasteners/fastener systems, aerostructures, and precision components; and cobalt, nickel, and titanium alloys. Additionally, the company distributes televisions and information; franchises and services quick service restaurants; distributes electronic components; and offers logistics services, grocery and foodservice distribution services, and professional aviation training and shared aircraft ownership programs. It also retails automobiles; furniture, bedding, and accessories; household appliances, electronics, and computers; jewelry, watches, crystal, china, stemware, flatware, gifts, and collectibles; kitchenware; and motorcycle clothing and equipment.

MKL Markel - 13%

Markel Group Inc., a diverse holding company, engages in marketing and underwriting specialty insurance products in the United States, Bermuda, the United Kingdom, and Germany. The company offers general and professional liability, personal lines, marine and energy, specialty programs, and workers' compensation insurance products; and property coverages that include fire, allied lines, and other specialized property coverages, including catastrophe-exposed property risks, such as earthquake and wind. It also offers credit and surety products, and collateral protection insurance products. In addition, the company offers transaction, directors and officers, and healthcare liability reinsurance; and specialty treaty reinsurance products comprising credit and surety, workers' compensation, marine and energy, public entity, mortgage default, aviation and space, agriculture, and discrete political violence and national terror pools. Further, it provides construction services, consumer and building products, transportation-related products, consulting services, and equipment manufacturing products, as well as healthcare, leasing, and investment services. Additionally, the company operates as an insurance and investment fund manager offering a range of investment products, including insurance-linked securities, catastrophe bonds, insurance swaps, traditional reinsurance contracts, industry loss warranties and other financial instruments; and program services. It also manages funds with third parties.

MITSY Mitsui Corporation - 12%

Mitsui & Co., Ltd. operates as an trading and investment company worldwide. The company engages in the manufacture and sale of steel products; steel processing, maintenance, and recycling activities; investment, development, and trading of mineral and metal resources, as well as resource recycling and industrial developing solutions; and upstream development, logistics, and trading of energy resources, such as natural gas/LNG, oil, coal, and uranium. It also offers power, gas, water, rail, and logistics systems; sales, financing, lease, transportation, and logistics services; and invests in plants, offshore energy development, ships, aviation, space, railways, and automotives, as well as machinery for mining, construction, and industrial use. In addition, the company provides basic chemicals and inorganic raw materials, functional materials, electronic materials, specialty chemicals, housing and lifestyle materials, agri-inputs, animal/human nutrition, and health products; and logistics infrastructures services, including tank terminal operation, as well as plastic recycling and next-generation energy, such as hydrogen and ammonia and forest resources businesses. Further, it engages in the food resources and products, merchandising, retail, fashion and textiles, wellness, healthcare, pharma, hospitality, and human capital businesses. Additionally, it is involved in the ICT, finance, real estate, and logistics businesses. The company was incorporated in 1947 and is headquartered in Tokyo, Japan. Mitsui E&P Italia B operates as a subsidiary of Mitsui & Co., Ltd.

NTDOY Nintendo - 12%

Nintendo Co., Ltd., together with its subsidiaries, develops, manufactures, and sells home entertainment products in Japan, the Americas, Europe, and internationally. It also offers video game platforms, playing cards, Karuta, and other products; and handheld and home console hardware systems and related software.

IMKTA Ingles Markets - 6%

Ingles Markets, Incorporated, together with its subsidiaries, operates a chain of supermarkets in the southeast United States. It offers food products, including grocery, meat and dairy products, produce, frozen foods, and other perishables; and non-food products, which include fuel centers, pharmacies, health and beauty care products, and general merchandise, as well as private label items. The company owns and operates a milk processing and packaging plant that supplies organic milk, fruit juices, and bottled water products to other retailers, food service distributors, and grocery warehouses. In addition, it provides home meal replacement items, delicatessens, bakeries, floral departments, and greeting cards, as well as broad selections of local organic, beverage, and health-related items. The company operates under the Ingles and Sav-Mor brand names.

Investment Thesis - Ingles Markets

Disclaimer: Pellom Capital Preservation LLC is a private family office registered in the state of Tennessee. Pellom Capital Preservation LLC is not a registered investment advisor with any governing or regulating body. Nothing in this website should be construed as a public offering or solicitation. We do not accept outside funds for our services.

MLR Miller Industries - 6%

Miller Industries, Inc., together with its subsidiaries, manufactures and sells towing and recovery equipment. The company offers wreckers that are used to recover and tow disabled vehicles and other equipment; and car carriers, which are specialized flat-bed vehicles with hydraulic tilt mechanisms, which are used to transport new or disabled vehicles and other equipment. It also provides transport trailers for moving various vehicles for auto auctions, car dealerships, leasing companies, and other similar operations. The company markets its products under the Century, Vulcan, Challenger, Holmes, Champion, Chevron, Eagle, Titan, Jige, and Boniface brands. Miller Industries, Inc. sells its products through independent distributors in North America, and Canada, Mexico; and through prime contractors to governmental entities. Miller Industries, Inc. was incorporated in 1990 and is headquartered in Ooltewah, Tennessee.

SHV iShares Short Treasury Bond ETF (cash) - 36%

I have bought and sold in and out of these holdings over the quarter (mostly as the result of employment change and the rotation of 401k assets), so I won’t misrepresent the facts and list a performance number here. Hopefully my portfolio will be more static in Q4 allowing for better tracking.

As you’ll see above, I am holding far more cash than I anticipated. I am genuinely uncomfortable with it, to be frank. I want to find more companies to buy, but I find the market historically overvalued at present and expect there to be ample buying opportunity in the future. Until that day, I’m satiated by following Warren Buffett’s lead and taking the 4-5% yield on short-term treasury bonds.

There are companies I’m researching and I would love your input throughout that process. I hope to use the Substack chat feature to post in real time as something catches my eye.

Ideas Worth Sharing

“The best way to get what you want is to deserve it.” - Charlie Munger

“History is just a collection of all the surprises we’ve encountered.” - Morgan Housel

“Panic is God’s way of telling us the worst is over.” - Mike Alkin

Conor Mac wrote a great piece on the problems at Burberry. This one will be on my watchlist for a while, I think. My gut is this is a 100+ year old company going through temporary mismanagement.

James Scurlock continues to write the most thought-provoking commentary on our current macroeconomic landscape:

The best book I read over the quarter was The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall Street by Justin Fox. — Goodreads Link

That’s all I have to report.

Thanks for reading and playing along,

Tyler Pellom